It was 2006, the first Office 2.0 Conference in San Francisco and I just met Jeffrey Walker, President of Atlassian. I had followed the company for a while (OK, I admit, had been a fan), met Mike, but this was the first time with Jeffrey, so we took our box lunch to a cozy little place away from the crowd and started to chat. Within minutes a VC Partner joined us, and so the usual “what are you doing” conversation started. Well, it wasn’t a conversation: Jeffrey talked, the VC listened. And in 5 minutes he was ready pull out the checkbook (sort of), when Jeffrey dropped the bomb:

It was 2006, the first Office 2.0 Conference in San Francisco and I just met Jeffrey Walker, President of Atlassian. I had followed the company for a while (OK, I admit, had been a fan), met Mike, but this was the first time with Jeffrey, so we took our box lunch to a cozy little place away from the crowd and started to chat. Within minutes a VC Partner joined us, and so the usual “what are you doing” conversation started. Well, it wasn’t a conversation: Jeffrey talked, the VC listened. And in 5 minutes he was ready pull out the checkbook (sort of), when Jeffrey dropped the bomb:

We’re actually not seeking funding. We’re fully funded. By customer revenues.

Seeing the VC’s face was priceless. After all, the cliche for startup success was to take funding. Which Atlassian did – 4 years later. But they do nothing by halves. $60 million or nothing! 🙂 But I am running ahead. Back to the early days.

I got to know Atlassian as the Wiki Company – having compared the few early business wikis, I came to the Conclusion that Confluence was the most robust, complete one. I’m probably not the most pleasant reviewer when I don’t like what I see – but I could simply not find anything to criticize with Confluence – it became the de facto industry standard for others to follow. That said Atlassian is /was about more then Confluence: their roots are in supporting developers, having started with a powerful bug tracker Jira, and growing to eight (?) products  organically and through acquisitions. Not being a techie, I don’t even understand most of these products – so the root cause of my infatuation with Atlassian was really their business model.

organically and through acquisitions. Not being a techie, I don’t even understand most of these products – so the root cause of my infatuation with Atlassian was really their business model.

There is nothing wrong with taking VC Funding, but risking everything to your last penny is what Entrepreneurship was originally all about, so it is simply refreshing to see a company to have made it solely on bootstrapping, beating the odds. Add to it great software that’s easy to buy, learn, use, sprinkle it with a good dose of transparency and great service, and you get a startup worth admiring. I’ve had lots of fun covering their early success and also learned a lot watching them:

- Atlassian taking in the world

- Atlassian Founders Become Australian Entrepreneur of the Year

- Flow vs. Structure: Escaping From the Document & Directory Jungle ( I badly need to revisit this subject)

- Choosing Your Customers: Smart Business or Arrogance?

- Software Startups: How to Sell to Enterprise in a Recession

Oh, and they gave me some of my funnier titles:

Sell Software – Ship T-Shirts (how come I don’t have them?)

Sell Software – Ship T-Shirts (how come I don’t have them?)- Atlassian Hiring Chief Heineken-taster

- Business Models and Right-brained Geeks

…’cause they like having fun, and I guess it’s contageous. But amidst all that fun they can sometimes be dangerous:-)

I tried to help them fill The Dream Job (no, I wanted that job:-)), help with their charitable promotion – hey, even put my http://www.cloudave.com/link/helping-atlassian-stimulus-package-towards-the-finish-line“>money where my mouth was. Then I had to write the most difficult post in my life, saying goodbye to Jeffrey, Atlassian President, musician, amazing person and fellow Enterprise Irregular.

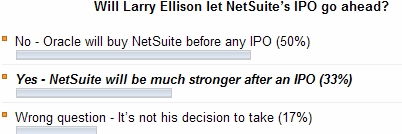

And today they taught me another lesson: don’t ever sit on a story. It expires. My unwritten story that I’ve been contemplating for a while was about two bootstrapped startups, both in software, amazingly successful that have sailed into IPO zone almost unnoticed. The second one is Zoho, which I consider to be approaching IPO-readiness, but I seriously doubt they would chose to go that way. But Zoho is our Sponsor, talking too much about them would look like ***ing up, so I’ll stop here. The day will come. But today is Atlassian’s day.

Why would a company that has profitably grown for 8 years need funding now? They want to grow more agressively, both in terms of geography and product coverage. That means acquisitions. They want to accelerate growth to above $100M revenue, which is what’s considered “IPO ready” nowadays.

But what drove me to the conclusion they were on the IPO-track even before the funding was deep in their culture.

But what drove me to the conclusion they were on the IPO-track even before the funding was deep in their culture.

Atlassian is always hiring, yet it’s difficult to get in. They are picky. It’s a “work-hard-play-hard” culture. Employees are well paid and the company spends lavishly on team fun. No wonder their revenue per employee ratio is high. But the team lives in Sydney and San Francisco, where there is an expectation that after a few years in a red-hot startup you get rich… The Founders probably no longer live frugally, but how to share the wealth with all employees without an exit? Funding accelerates the path to exit and my even bring interim liquidity critical to keep the team around. I agree with Ben in that respect.

$60 million is a lot of money, in fact Accel Partners claim it is the largest investment they’ve ever made in the software business. But there’s a whole world of difference in picking it up as a mature, profitable company or a fledgling startup. Some of Atlassian’s competitors picked up a third of this amount at early stages and probably had to give up three times as much equity as Atlassian did. Bootstrapping has paid off, after all.

$60 million is a lot of money, in fact Accel Partners claim it is the largest investment they’ve ever made in the software business. But there’s a whole world of difference in picking it up as a mature, profitable company or a fledgling startup. Some of Atlassian’s competitors picked up a third of this amount at early stages and probably had to give up three times as much equity as Atlassian did. Bootstrapping has paid off, after all.

Oh, about that $60M T-shirt – you really have to read it over @ Atlassian. After all, this is a SFW blog:-)

Update: I’m speechless. What’s this? Sour grapes?

(Cross-posted @ CloudAve)

Yes, I like LinkedIN, and am one of the very early users, from the early days before social networks become trendy. Simply because,

Yes, I like LinkedIN, and am one of the very early users, from the early days before social networks become trendy. Simply because,

Recent Comments